Loan Agreements and Insurance: Lender and Borrower Duties in Art

You’ve just secured a major loan for that rare Renaissance painting or the limited-edition contemporary sculpture. The money is in the bank, but the real work is starting now. In the high-stakes world of fine art financing, the contract you sign isn’t just about interest rates and repayment schedules. It’s a binding document that dictates who protects the asset if it gets damaged, stolen, or destroyed.

Whether you are a private collector using art as collateral for a liquidity line or a gallery borrowing from an institution, understanding the split of duties between lenders and borrowers is critical. Get this wrong, and you could be on the hook for millions in uncovered losses. Let’s break down exactly how these agreements work and where the liability lines are drawn.

The Core Structure of Art Loan Agreements

When we talk about art loans, we aren’t usually discussing a standard mortgage. These are specialized financial instruments often referred to as art-secured lending. The central entity here is the Art Loan Agreement, which is a legal contract governing the use of fine art as collateral for a financial loan. Unlike a house, art doesn’t have a standardized appraisal process, and its value can fluctuate wildly based on market trends, provenance discoveries, or even changes in public taste.

This volatility creates a unique risk profile. The lender needs assurance that the collateral will retain enough value to cover the outstanding debt. The borrower needs access to cash without having to sell their prized possession. The agreement bridges this gap by establishing strict rules for custody, valuation, and insurance. If you’re new to this, think of it less like a bank loan and more like a high-security storage deal with a financial twist.

Lender Duties: Due Diligence and Collateral Management

It’s easy to assume the lender’s job ends once they hand over the check. In reality, their duties are extensive and ongoing. The primary responsibility of the Lender in an art transaction is the financial institution or individual providing funds, responsible for verifying collateral value and enforcing security terms. falls under two main buckets: verification and protection.

First, the lender must conduct rigorous due diligence. This isn’t just about getting an appraiser’s number. They need to verify the authenticity of the piece. A fake Picasso might look real, but it has zero collateral value. Lenders typically require independent authentication from recognized experts or auction houses. They also check the title history to ensure there are no liens or ownership disputes.

Second, lenders dictate the storage conditions. Most agreements require the art to be kept in a bonded, climate-controlled facility. Some lenders insist on holding the physical asset themselves in their own vaults. Others allow the borrower to keep the piece at home or in a private museum, provided it meets specific security standards (like 24/7 monitoring and fire suppression systems). The lender’s duty is to ensure these standards are met through regular inspections or third-party audits.

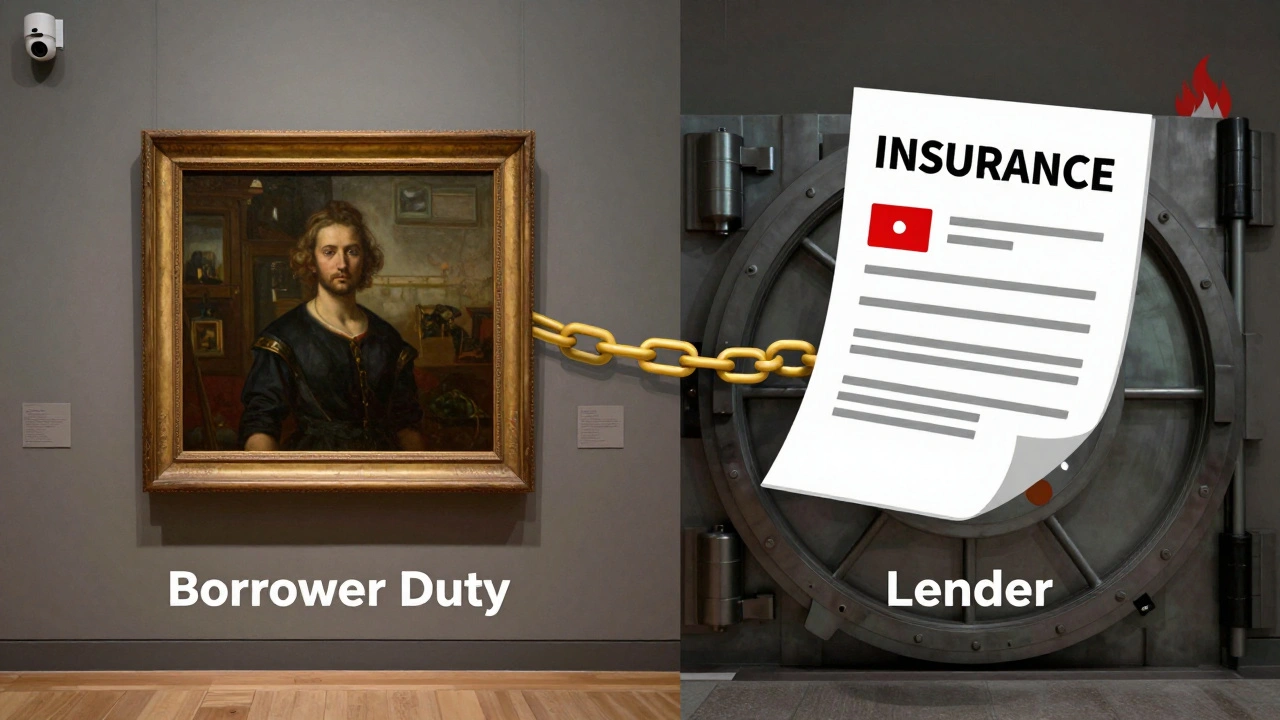

Borrower Duties: Insurance and Maintenance

If the lender owns the security, the borrower owns the risk of daily management. Your duties as a Borrower include the art owner who receives funds and is responsible for maintaining the asset's condition and securing adequate insurance coverage. are centered on preserving the asset’s value. The most critical of these is insurance.

You cannot simply add the artwork to your homeowner’s policy. Standard policies rarely cover high-value fine art adequately, and they often exclude risks like accidental damage during handling or transit. You need a specialized fine art insurance policy. This policy should be "all-risk" rather than "named-peril," meaning it covers everything except what is explicitly excluded. Common exclusions might include war, nuclear events, or gradual deterioration due to poor maintenance.

Who pays for this insurance? Usually, the borrower does, but the cost is factored into the loan’s carrying costs. More importantly, the lender must be named as the "loss payee" or "mortgagee" on the policy. This means if the art is destroyed, the insurance check goes directly to the lender to satisfy the debt, not to you. Any remaining proceeds after the loan is paid off then go to you.

Valuation Methods: Appraised vs. Market Value

A major point of contention in loan agreements is how the collateral is valued. There are two primary methods, and they serve different purposes:

- Appraised Value: This is the expert opinion of what the art is worth at a specific moment in time. It’s used to set the initial Loan-to-Value (LTV) ratio. For example, if a painting is appraised at $1 million, the lender might only lend 50% ($500,000).

- Market Value: This is what the art would actually sell for at auction today. This is crucial for liquidation scenarios. If you default on the loan, the lender needs to know the market value to determine how quickly they can sell the asset to recoup their losses.

The gap between these two values is where risk lives. Art markets can be illiquid; selling a niche piece might take months. Lenders account for this by keeping LTV ratios low, often between 30% and 50%. As a borrower, you need to understand that your equity in the piece shrinks as the loan balance decreases, but the collateral requirement remains fixed until the loan is repaid.

Risk Allocation: What Happens When Things Go Wrong?

Let’s talk about the worst-case scenarios. Who pays if the painting is scratched? Stolen? Destroyed by flood? The answer lies in the "Risk of Loss" clause of the agreement.

| Event | Borrower Responsibility | Lender Action |

|---|---|---|

| Minor Damage (Scratches) | Repair costs; may trigger re-appraisal | Review repair quality; adjust LTV if value drops |

| Total Loss (Fire/Theft) | Ensure insurance claim is filed promptly | Receive insurance payout; apply to loan balance |

| Market Decline | May need to provide additional collateral | Issue margin call or demand partial repayment |

| Default on Payment | Lose ownership of collateral | Seize and sell art to recover funds |

Note the "Margin Call" scenario. If the market value of your art drops significantly-say, due to a scandal involving the artist or a broader economic downturn-the lender can demand you put up more collateral or pay down the loan. This is similar to stock trading margin calls. It’s a vital protection for the lender, but a potential trap for the borrower who might not have the liquidity to respond.

Transit and Exhibition Risks

Many borrowers want to display their art. Maybe it’s in your home office, or perhaps you’re lending it to a museum for a show while still holding the loan. This introduces "transit risk." Moving fine art is dangerous. Vibrations, temperature shifts, and human error can cause irreversible damage.

Your duties expand here. You must use professional fine art shippers, not standard moving companies. The shipping company must carry their own liability insurance, but this is secondary. Your primary insurance policy must remain active during transit. Many lenders prohibit movement without prior written consent and proof of insured transport. Never move collateralized art without notifying your lender first.

Navigating the Legal Landscape

Art law is complex because it intersects with property law, contract law, and international trade regulations. If the art crosses borders-for instance, if you’re a US-based borrower storing the piece in Europe-you enter the realm of customs bonds and VAT implications. The lender will likely require you to handle all import/export licenses. Failure to do so can result in the seizure of the art by government authorities, leaving the lender with nothing.

Additionally, consider the concept of "perfecting" the lien. In legal terms, this means the lender has publicly recorded their interest in the art. In many jurisdictions, this involves registering the lien with a national art registry or equivalent body. If the lender hasn’t perfected their lien, and you try to sell the art to someone else, that buyer might get clear title, leaving the lender unsecured. As a borrower, you should ensure this step is completed to avoid future legal ambiguities.

Practical Tips for Borrowers

To protect yourself when entering these agreements, keep these points in mind:

- Read the Insurance Exclusions: Make sure "accidental damage" is covered. Many standard policies exclude this, which is a huge risk for displayed art.

- Clarify Re-appraisal Triggers: How often will the lender re-evaluate the art’s value? Annual is standard, but frequent re-appraisals can lead to unexpected margin calls.

- Negotiate Storage Flexibility: If you want to display the art, negotiate terms that allow it under strict security guidelines rather than requiring vault storage.

- Understand Default Terms: Know exactly what constitutes a default. Is it missing one payment? Or is there a grace period? Clarity here prevents accidental foreclosure.

Conclusion: Balancing Access and Security

Loan agreements in the art world are tools for unlocking liquidity without sacrificing ownership. However, they shift significant operational burdens onto the borrower. You become the manager of a high-value, fragile asset while simultaneously managing a financial obligation. By clearly defining duties around insurance, storage, and maintenance, both parties can mitigate risk. The key is transparency. Ensure your insurance aligns with the lender’s requirements, and never underestimate the importance of proper documentation and professional handling. When structured correctly, these agreements allow collectors to enjoy their art financially and aesthetically, without fear of catastrophic loss.

What happens if my art is stolen while I have a loan against it?

If the art is stolen, you must immediately notify your insurer and the lender. Because the lender is listed as the loss payee on your insurance policy, the insurance payout will go directly to them to offset the outstanding loan balance. If the insurance payout exceeds the loan amount, the surplus is returned to you. If it falls short, you may still owe the difference depending on your loan terms.

Can I display art that is used as collateral for a loan?

Yes, but only if permitted by the loan agreement. Many lenders allow display in secure, climate-controlled environments like private homes or museums. However, you must maintain comprehensive insurance coverage and meet specific security standards, such as having alarm systems and professional lighting. Always get written permission before changing the location of the collateral.

How often is the value of my art re-appraised?

Re-appraisals typically occur annually or biannually, depending on the loan term and the volatility of the art market. Some lenders may request immediate re-appraisals if there is a significant change in the market or if the art suffers any damage. These updates ensure the Loan-to-Value (LTV) ratio remains within acceptable limits.

What type of insurance is required for art-backed loans?

You need a specialized "all-risk" fine art insurance policy. This covers theft, fire, water damage, and accidental breakage. Standard homeowner’s policies are insufficient. The policy must list the lender as the loss payee and cover the full appraised value of the artwork. Transit insurance is also required if the art moves locations.

What is a margin call in the context of art loans?

A margin call occurs when the market value of your collateralized art drops below a certain threshold relative to your loan balance. The lender may demand that you provide additional collateral (more art or cash) or make a partial loan repayment to restore the agreed-upon Loan-to-Value ratio. Failure to comply can lead to default.